Consumer Price Index, Inflation Rate and 2023 Mortgage Rates

On October19, 2022 Stats Canada posted September’s data to the consumer price index (CPI), and updated the inflation rate.

For the 4th month in a row, the Consumer Price Index posted results in-line with previous months, showing no significant gain. This decreased the inflation rate from 7.0% to 6.9%.

Now I know 0.1% seems like a miniscule decrease, but if we can stay on this path we’ll see large decreases in the inflation rate starting in January through May.

**To learn how the inflation rate is calculated please see the formula outlined below.

As you can see from the last 4 months of data, aggressively raising the interest rate has slowed the economy and kept the CPI index within a range of +/- 0.5. If the bank can maintain this stalled price growth going forward, we will see the inflation rate come down quickly in the first half of 2023.

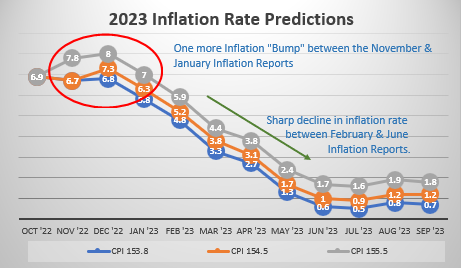

Expected Inflation Rate for 2023

If (big if) the Consumer Price Index doesn’t exceed 153.6 (current CPI is 152.7) the expected inflation rate for 2023 is as follows:

** A conservative CPI of 153.6 was used for this chart.

What happens when inflation gets back to the 2% target? Will interest rates decrease immediately?

Once the Bank of Canada hits their target (hopefully by summer 2023 if all goes well), it is unlikely we will see any major decreases in the variable interest rates for a few months. The Bank will want to keep interest rates elevated for sometime afterwards to ensure inflation doesn’t return.

However, there is some good news! As the inflation rate drops, bond yields will decrease as well. The drop in bond yields will then cause the fixed mortgage rates to decrease. The first rates to decrease will be the 5-year fixed, then 4-year fixed and so on.

What to expect in the coming months?

Expect at least 2-more rate hikes this year. Bank of Canada will likely increase the interest rate by 0.50% – 0.75% on October 26, and will likely see another increase on December 7th.

The Consumer Price Report/Inflation Rate Reports releasing on November 17, December 21, and January 17 will provide us with the data we need to know to ensure we are on the correct path.

The Bank is looking for a significant drop in the inflation rate, but (if all goes well) we wont see this drop until the January CPI Report.

How to Calculate the Inflation Rate using the CPI Report

Using the Consumer Price Index graph above, we calculate the inflation rate on a yearly basis.

The formula to calculate the rate of inflation is: (X – Y) / Y * 100 = Inflation Rate

- X is the current month

- Y is the base month

Example

X – Current Month: September 2022: 152.7

Y – Base month: September 2021: 142.9

Equation: (152.7 – 142.9)/142.9 * 100 = 6.857%, we round up to get an Inflation Rate of 6.9%

Links to the CPI Report Data

Do you have any home finance questions I can help answer? Let’s connect!

Adam Sale Mortgages

778-215-4121