Does it make sense to go with the cheaper Variable Rate mortgage or the more expensive Fixed Rate mortgage?

It all depends on what the buyer is planning on doing with the property.

Scenario 1 – Buy and Flip

When purchasing a property to flip the variable rate mortgage adds flexibility to pre-pay the mortgage without incurring outrageous pre-payment penalties seen on fixed rate mortgages.

The pre-payment penalty for a variable rate mortgage is 3-months of interest. If mortgage payments are $2,000/m, the interest payment will be at most 50% of the payment ($1000). If we multiply this amount by 3-months the pre-payment penalty would equal $3,000. Which is a much less than the fixed-rate’s Interest Rate Differential penalty.

Scenario 2 – Buy and Hold for 3 years or More

Bank of Canada has mentioned on several occasions they will be keeping interest rates low until the end of 2022/early 2023. Based on this information it may make sense to go with a fixed rate mortgage if the buyer is planning on living in the property for 3-5 years.

The current premium for a fixed rate mortgage vs variable rate mortgage is approximately 0.25%.

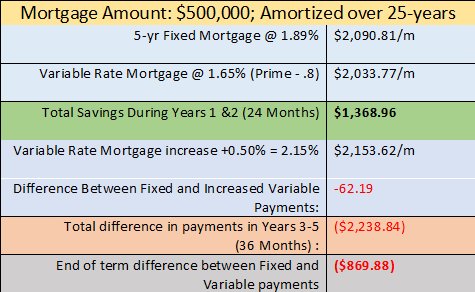

On a $500,000 mortgage the payments are as follows:

Monthly Fixed Payment @1.89%: 2,090.81

Monthly Variable Payment @ 1.65%: $2,033.77

A difference of $57.04/m! – If we expected interest rates to remain low for the full 5 years this would result in $3,422.40 of savings!

However, according to Bank of Canada we expect interest rates to start rising in Year 3. It is likely interest rates will rebound by 0.50%-0.75%.

How quickly these rates rise will be the determining factor on whether Variable vs Fixed is the better option from a savings perspective.

Following the financial crisis that started in early January 2008, interest rates rose by 0.75% in the 4-month period from June-September 2010. Canada saw a period of low interest rates for almost 30-months!

If you found this chart interesting, and would like another scenario explored, please contact me at adamsale@dominionlending.ca or @778-215-4121

Cheers,

Adam