Yesterday (March 10) the Bank of Canada kept their word on keeping the overnight interest rate unchanged. They’ve mentioned numerous times their plan is to keep the target interest rate unchanged until 2023, at which point they believe the economy will show decreased unemployment numbers and the economy will be operating near capacity.

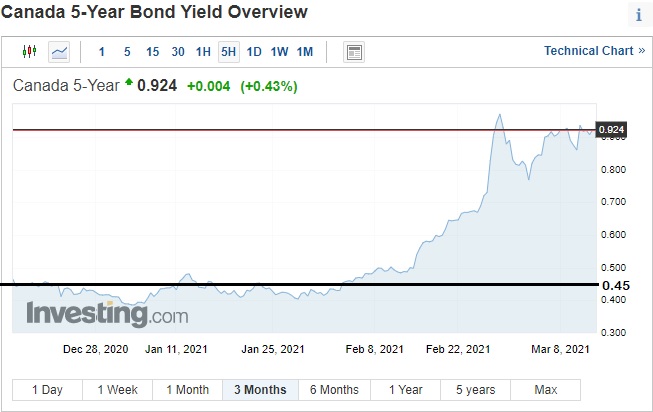

However, the bond market’s yields (interest rates) are increasing since January which is driving the fixed-rate mortgages to highs not seen since the pandemic started a year ago. The 5-year bond yields have increased by half a percent since mid-January, and the 5-year fixed-rate mortgages have followed suit.

5-year bond yield

Where’s the Opportunity for the Lowest Mortgage-Rates?

The opportunity for the lowest mortgage rates is in the variable mortgage product and the 3-year fixed mortgage product.

Variable rate mortgages are at a significant discount, and vary between 1.45-1.85% depending on the type of mortgage. It is unlikely the variable rate mortgages will decrease further, and expect the interest rate to rise in 2023 when the Bank of Canada increases their rates. I feel a realistic hike throughout 2023 would be between 0.5%-0.75%.

Any purchaser looking for flexibility to time the market and sell their property at the peak price should consider the variable rate mortgage for its low-penalty.

Homeowners wanting a stable payment can find the cheapest rates in the 3-year fixed-term mortgage products. 3-year bond yields are not increasing as rapidly as the 5-year bond yields so expect many 3-year term mortgage specials to appear in the coming weeks, several lenders are already offering insured specials at 1.59%.

First-time homebuyers purchasing a starter home should consider the 3-year fixed-rate mortgage as it offers flexibility to sell and move into something larger at the end of 3-years without incurring penalties.

3-year bond yield

Deciding which mortgage product to use should always depend on what your goal is for the property in 3-5-10 years. Often the lowest-rate mortgage product is not the cheapest product for your personal scenario.